"The S&P bounced beautifully, straight into its 200-day moving average. This week, the Strait stays shut, Trump's deadline expired unanswered, and March CPI drops Thursday. The market is in the in-between. That never lasts long."

— Proflex Panel

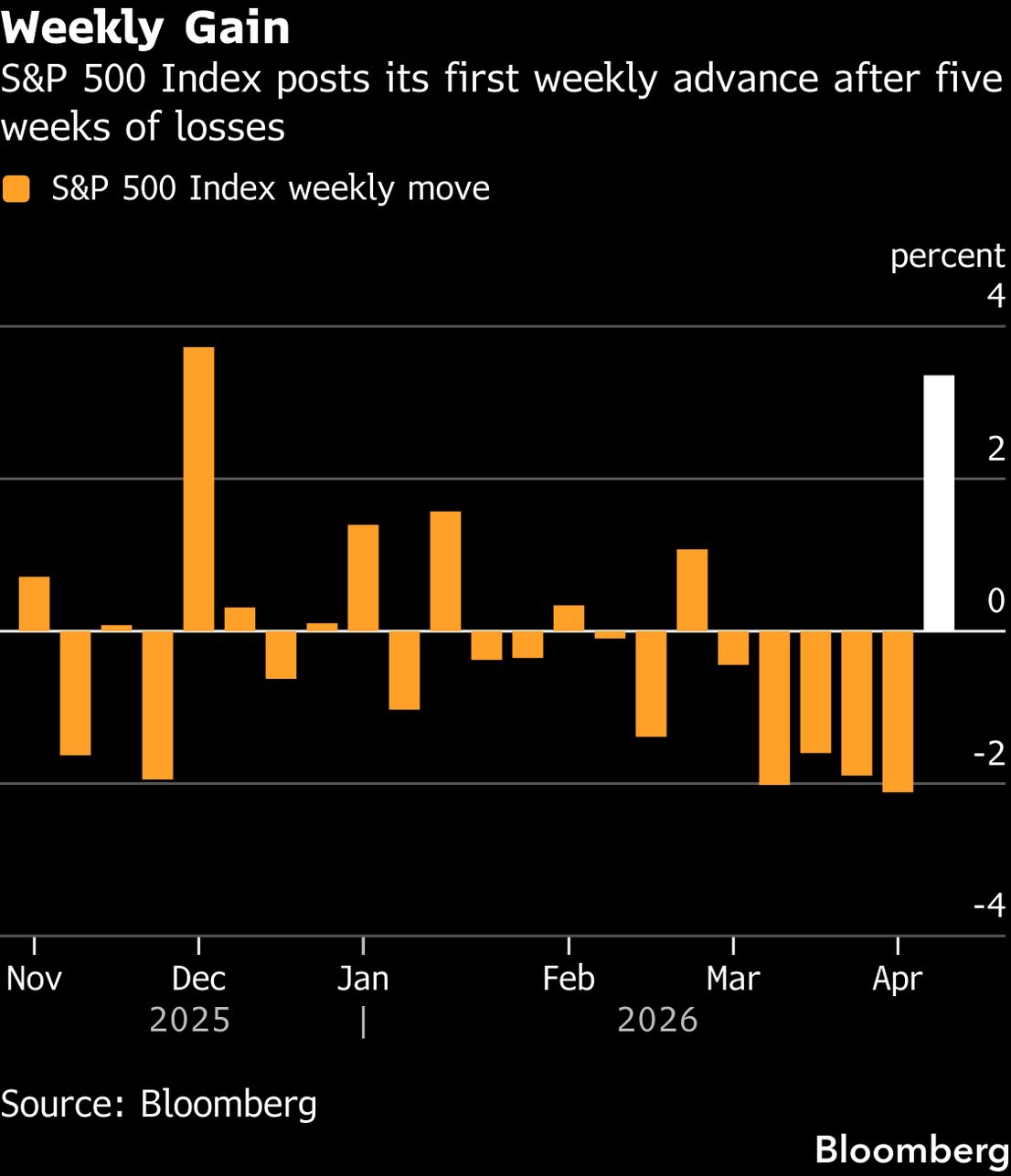

Last week gave bulls what they needed: the S&P 500's first weekly gain in six weeks, up 3.4% — its best week in four months.

Panic selling absorbed five weeks of war-driven losses, short sellers covered, and the index clawed back to 6,582 before markets closed for Good Friday.

But the bounce ran straight into a wall.

The 6,600–6,660 zone — where the 200-day moving average converges with the war's descending trend line — rejected every attempt to close above it. The Thursday intraday high barely tagged 6,601 before pulling back. As we outlined in Week 10 when 6,700 was the must-hold level, these zones don't yield cleanly because they require a catalyst. This week, the calendar delivers several.

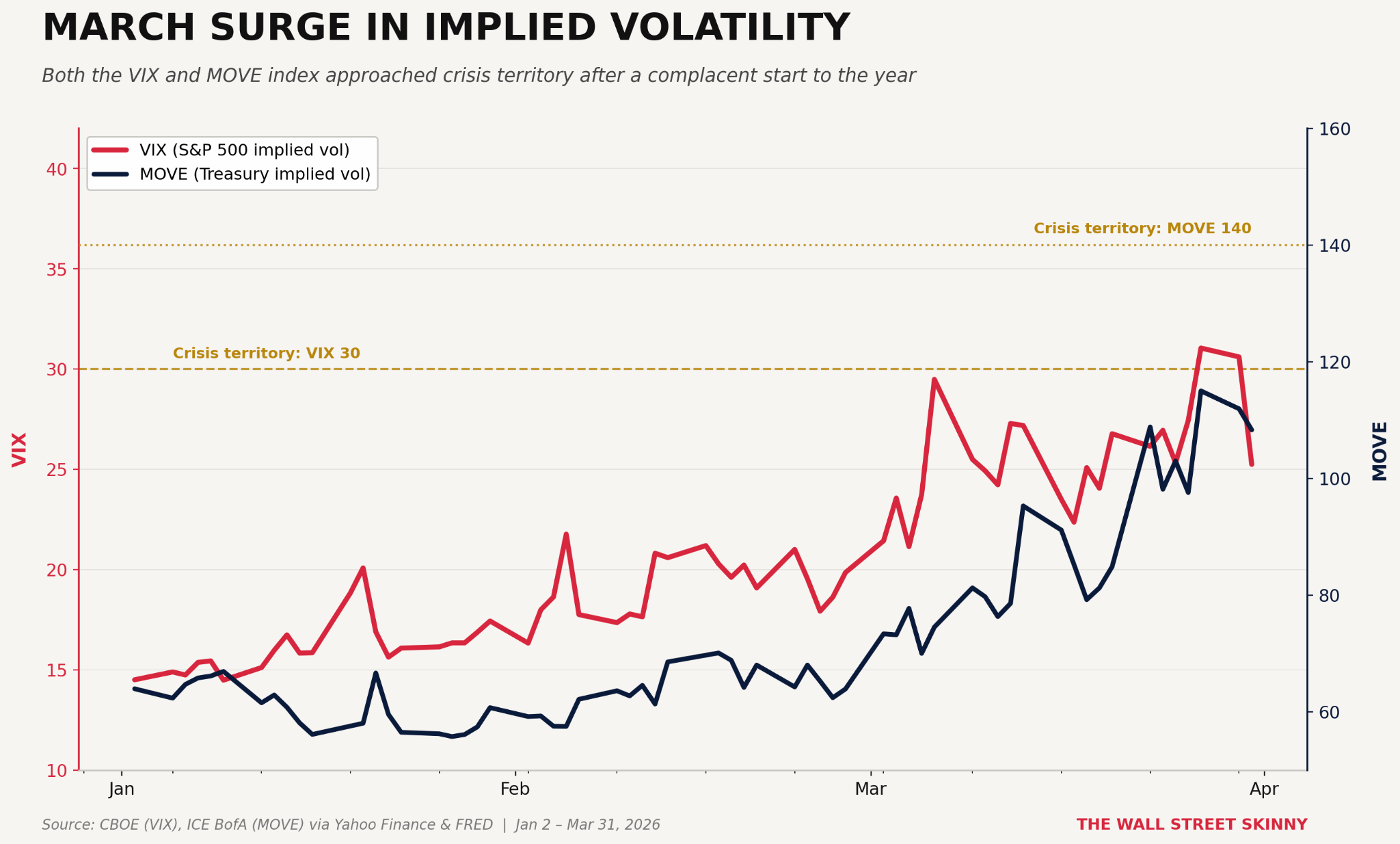

Three collision events are converging as markets reopen this week: 1) Trump's April 6 ultimatum for Iran to reopen the Strait of Hormuz expired this morning with Tehran formally rejecting it. 2) Brent is holding its ground And March CPI — the first inflation reading to capture the full oil surge — drops Thursday. 3) The VIX has cooled from its panic peak near 30 to 24-25, but still elevated. The war premium is still fully embedded.

Insights from Proflex Macro Call

The central theme from this week's call was straightforward: the bounce was real, but do not mistake exhaustion for resolution. Raman walked through the key dynamics in detail.

On the S&P 500: the 6,600 level is now the new line. We called 6,700 as the must-hold in Week 10 — that floor broke, the market found a new base, bounced, and has now met resistance at exactly the 200-day moving average and the war's downtrend line. Clearing it requires a catalyst, not just optimism. The VIX cooling from ~30 to 24.54 is healthy — we noted in Wk 11 that a VIX of 30 was pricing an unsustainable 2% daily move — but at 24-25, we are still well above the steady-state 200-day average of ~18. The war premium is priced in. It hasn't left.

On oil and the Strait: Ignore the speeches. Trump's April 1 address ("Operation Epic Fury") was framed by Raman as a sales pitch for US crude exports, not a strategic military update. What matters is whether ships are moving — and the early signs of an Oman coastal corridor (first vessels transiting this week) is the real signal the market hasn't fully processed. If that trickle becomes a pipeline, oil comes down fast. You can watch the complete recording here:

Proflex All-Access With 3+ years beating benchmarks, All-Access is a way for informed investors to learn how to trade & think like Institutions do, at a fraction of the cost.

Gain Complete Access to our full research suite, curated from over 50+ analyst forums, Real-time Trade Alerts & Updates for Growth & Income Opportunities —and join a thriving investor community alongside Big Tech Executives and fund managers from Silicon Valley and beyond.

The Resistance Test: 200-Day Moving Average or Roll Over

The S&P 500's best week in four months was also the market bumping into its most watched technical ceiling. The 200-day moving average sits at ~6,641–6,687 — the index closed April 2 at 6,582.69, below it. Markets were closed Friday (Good Friday) and reopen Monday into whatever war headlines the long weekend delivers.

We believe the VIX at 24-25 reflects a market that has digested panic but hasn't resumed confidence. Steady-state for a non-crisis VIX is around 18 — we're still 6 points above that. Dealer hedging pressure has eased; it hasn't reversed.

Two scenarios define the week ahead: A sustained daily close above 6,660 changes the medium-term setup materially — the path to 6,800+ opens and the war correction starts looking like a base. If resistance holds and escalation news re-enters Monday's open, a retest of the 6,400–6,300 zone (September/November 2025 lows) is the next logical support.

Proflex View: The oversold bounce cleared the panic — it didn't clear the problem. 6600 is the line between "relief rally" and "resumption." The 200-day moving average is where every seller who missed the first exit is waiting. A weekly close above 6,660, on volume, changes the narrative. Until then, this is a zone to watch, not a zone to chase.

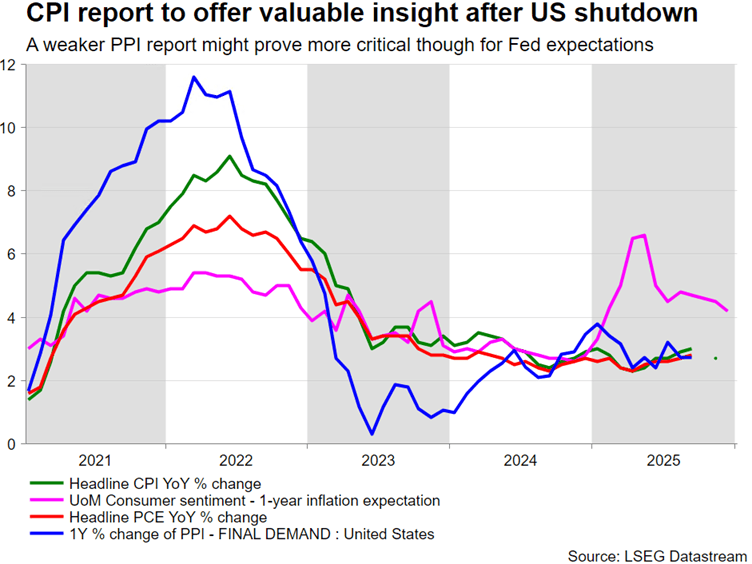

CPI Thursday: The Number That Could End Rate Cut Hopes

March CPI releases Thursday, April 10. This is the most important macro data point of the week and possibly of the month.

February CPI came in at +2.4% YoY with core at +2.5%. That was the last clean pre-war reading. Since then, Brent moved from $75 to ~$110. Core PCE for January (most recent) was already at 3.06% — above the Fed's 2% target. The pass-through is not hypothetical, it's clearly in the pipeline.

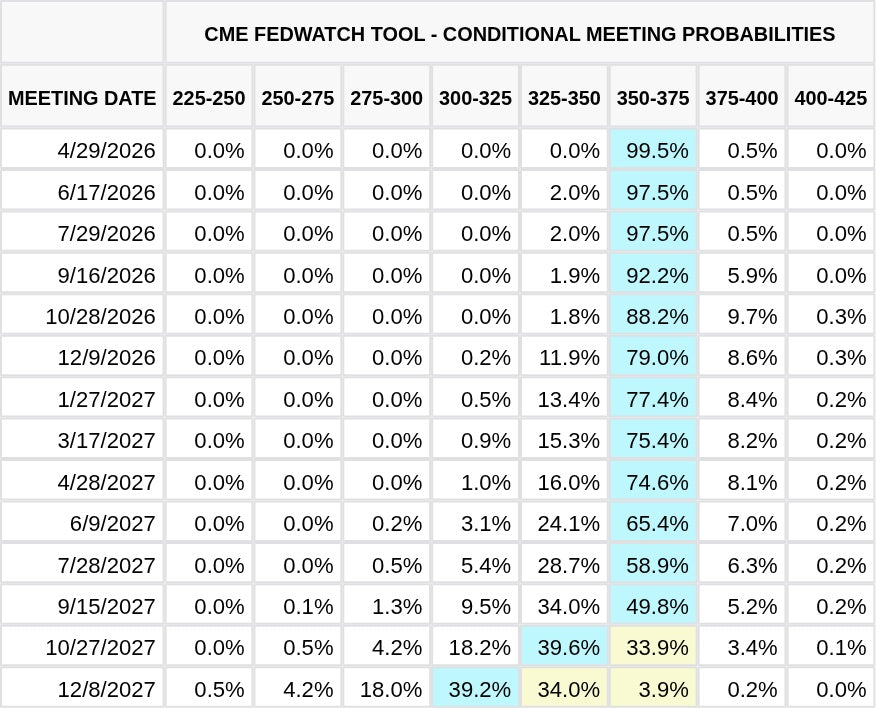

The Fed meets April 28–29. Markets price a 99.5% probability of a hold at 3.50–3.75%.

But the divergence on what comes after is wide and widening: 1) JPMorgan now forecasts zero rate cuts in 2026; Goldman still models two (June + September). 2) Fed Governor Logan remains hawkish on inflation;Governor Bowman is watching February's 92,000 job losses and arguing for three cuts. 3) The 10-year yield has pulled back from the 4.5%+ danger zone to 4.31% — a relief, not a clearance. DXY hovers near 100.

Proflex View: A March CPI above 3.0% closes the door on June cuts, even for Goldman. That repricing hits the long end of the yield curve immediately. The critical sub-figure is core ex-energy: if oil bleed-through shows up in core, the stagflation thesis goes from Wall Street debate to mainstream consensus. Watch core. That's the number inside the number.

The Earnings Counter-Narrative: Tech Got Cheaper

While the war dominates headlines, a structural counter-narrative is quietly building. Factset’s update for last week saw 2026 SPX earnings growth expectations increasing to +17.4%, up +1.1% the past two weeks and +2.6% since the start of the year.

Like in 2025, Tech is expected to lead earnings growth +37.3% (up +8.7% since the start of the year) followed by Materials +29.4% and Energy +26.0% (up from +6.4% as the start the year), the only three sectors expected to come in above the SPX average

Tech sector earnings expectations stand at +23.7%, with revenue growth of +21.2%. The AI capex cycle hasn't flinched: combined hyperscaler spending in 2026 is now $650–700 billion — Amazon at $200B, Alphabet at $175–185B, Meta at $115–135B, Microsoft at ~$145B. That's a 36% increase over 2025's $381 billion. None of it has been pulled back.

The S&P 500 forward P/E has compressed to 20.96 — essentially at the 5-year median of 21.12. As we've maintained since Week 08 update, the tech bottom forms before the macro resolves. The correction handed investors a re-entry into quality AI names at fair value rather than a premium.

Bank earnings kick off next week: Goldman Sachs (April 13) JPMorgan, Citi Wells Fargo (April 14) These will be the first signals on whether investment banking activity and credit quality have held up beneath the war noise. Tesla will be one of the most important earnings to watch as it reports April 22 with analysts expecting +60% YoY EPS growth.

Proflex View: AI isn't over and the war correction handed a rare re-entry. The capex cycle cannot be cancelled by an oil shock; these are multi-year infrastructure commitments. Bank earnings starting April 13 are the next catalyst cluster. If they show healthy pipelines, it signals the underlying economy hasn't cracked despite the war premium.

Bitcoin & Gold: Same Safe Haven Category, Different Signal

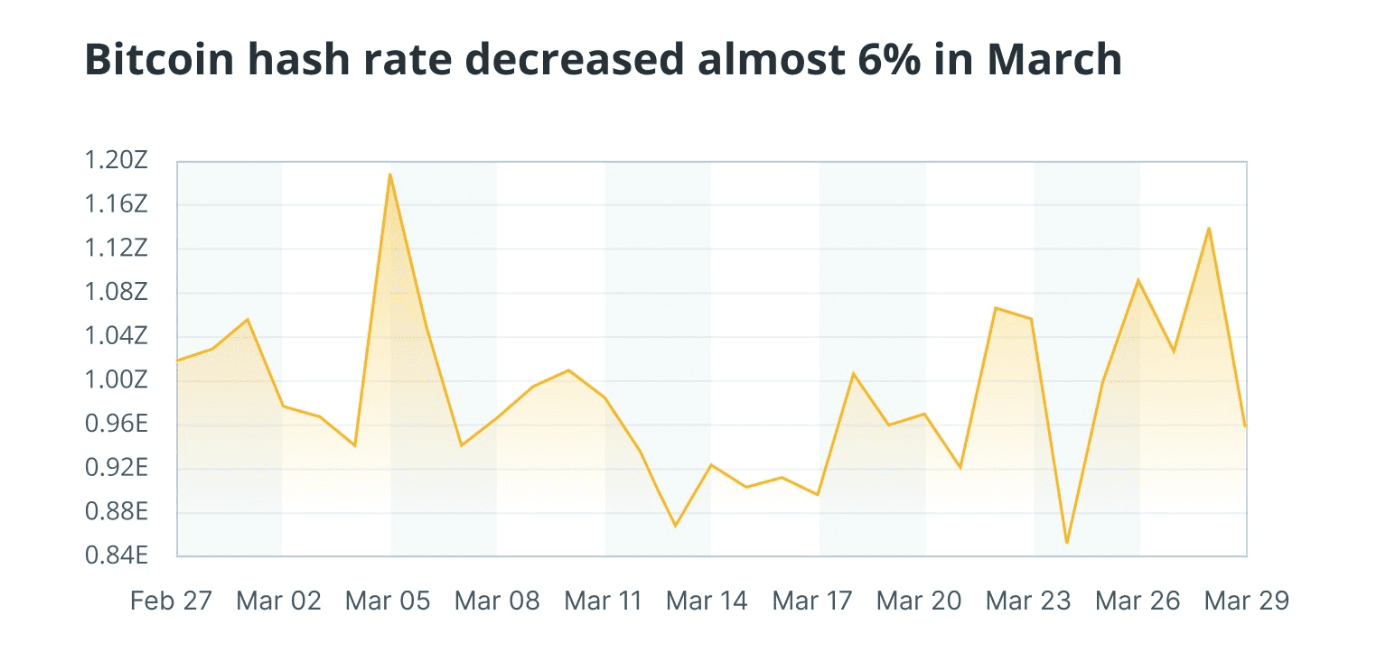

Bitcoin is consolidating in the $65,000–$70,000 zone. The asset's resilience is partly structural: US-Israeli strikes on Iranian mining infrastructure cut global Bitcoin hashrate by ~6% in March removing a persistent seller from the market.

Iran had accounted for an estimated 3–7% of global hashrate since 2019.

Long-term holders have been accumulating since mid-January 2026 — the first net accumulation phase since July 2025. MicroStrategy holds 762,099 BTC at an average cost of $75,694. Michael Saylor's "Back to Work" post on April 5 is his standard signal ahead of a new purchase announcement.

Bitcoin miners, however, remain structurally underwater: average production cost is ~$79,995/BTC versus the current spot price of ~$67k — a margin squeeze that has already triggered miner selling of 15,000+ BTC in Q1.

Gold sits at $4,674/oz, consolidating after its speculative excess cleared. China has purchased gold for 16 consecutive months, building reserves to 2,309 tonnes — now 10% of its total FX reserves. The World Gold Council reports 43% of global central banks plan to increase gold holdings over the next year. This is what we describe as a decade-long allocation shift away from dollar-denominated reserves accelerating under war conditions.

Proflex View: Bitcoin's consolidation reflects a healthy base: panic sellers washed out. The key tell is a sustained weekly close above $70,000 that confirms the base held and opens the next leg. Gold stays structurally bullish but with heightened volatility. Both assets are functioning exactly as they should in a deglobalization environment.

🔍 What We're Watching

March CPI (Thursday, April 10) — first oil-contaminated inflation print; the core ex-energy sub-figure is the one to watch

Oman corridor transit volumes — the real Hormuz signal; each additional vessel is a data point toward logistics resolution

Iran's escalation posture — April 6 deadline rejected; ground invasion risk into Monday's market open

S&P 500 weekly close vs 6,660 — above changes the medium-term setup; below keeps the range intact

Bank earnings (April 13–15) — Goldman, JPMorgan, Citi, BofA; investment banking pipeline = economy health check

MicroStrategy BTC announcement — Saylor's "Back to Work" signal; watch for confirmed purchase

🧭 Proflex Playbook – Discipline Over Direction The market is caught between a geopolitical crisis it can't model and a structural expiry event it can time to the hour. This is a week for tactical discipline. Our conviction stays anchored in the data:

Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

Proflex All-Access: Your Market Compass

Explore the financial markets with Proflex All-Access, your comprehensive resource for deeper market understanding and active participation. This premium service offers subscribers exclusive insights and actionable investment advice, giving you a significant edge in various market conditions.

Proflex All-Access provides detailed analyses and recommendations to optimize your investment strategy. Our specialized newsletters include:

• Growth Gazette (Contains Crypto Pulse) : Aimed at achieving above-market returns for aggressive portfolio growth.

• Income Insider: Focused on conservative strategies and income generation for yield-seeking investors.

Until next week, — The Proflex Team Trusted Macro Insights. Calm Investing. Tactical Trades.

Elevate your financial IQ

ProFlex® by Blockstart Research Legal Disclosures

ProFlex® by Blockstart Research, the premium newsletter product series, provides informational and educational content only and does not offer personalized investment advice or establish a fiduciary relationship. While we rely on reliable sources and research, the information is not tailored to individual financial situations. Readers are urged to consult qualified financial professionals before making investment decisions. We do not guarantee the accuracy, completeness, or timeliness of the information and are not responsible for any investment decisions based on this newsletter. Investing carries risks, and past performance doesn't predict future results. By accessing this newsletter, you acknowledge that we are not liable for actions or decisions resulting from its content. Please conduct due diligence and seek professional advice as needed.

Proflex Institutional Research Series

Elevate Your Investment Game!

ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.