ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.

Proflex Wk Apr 6-10 — Ceasefire Collapses, Earnings Season, AI’s Infrastructure Wall

|

Proflex Market Update - Week 6-10 April, 2026 Negotiation Deadline Expired | CPI Thursday | Earnings Preview

"Last week gave markets the thing they had been waiting for — a ceasefire window. The weekend took it back. The US just traded diplomacy for a naval blockade, and oil is reacting accordingly."

— Proflex Panel

Last week we saw the S&P 500 surge 3.6% — its best week in months as markets priced in a ceasefire window.

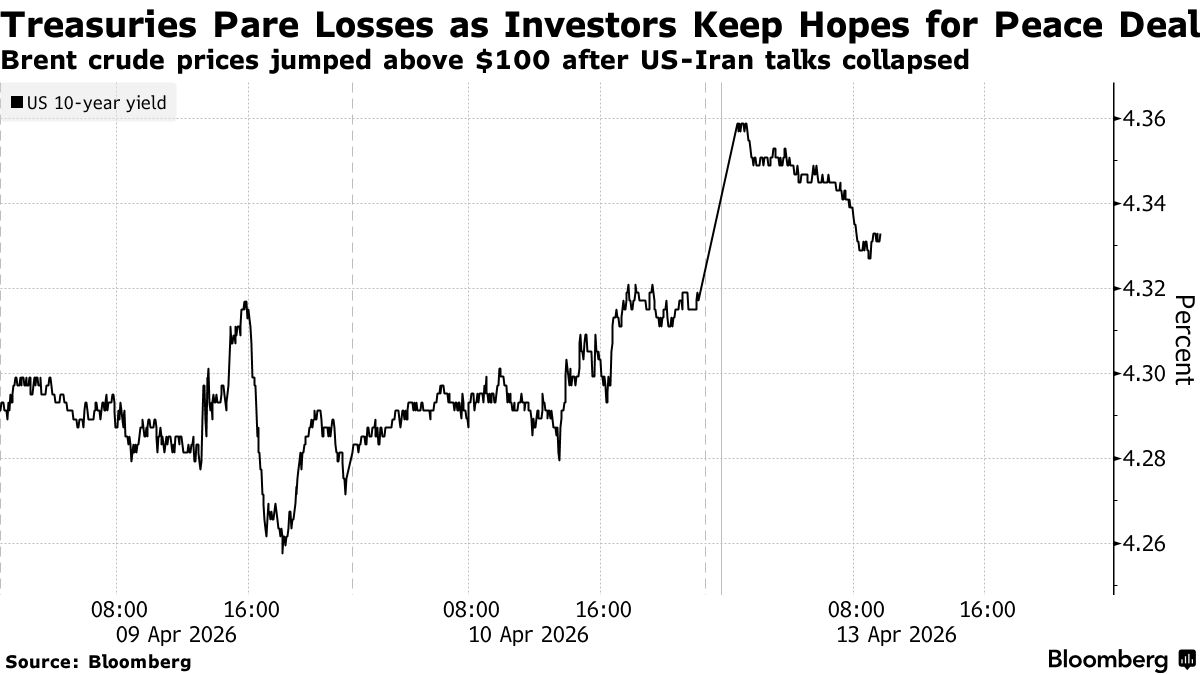

During the weekend, talks between the US and Iran collapsed over the weekend with no alignment on terms. Trump responded within hours, ordering a naval blockade of the Strait of Hormuz to prevent Iran from selectively allowing vessels through.

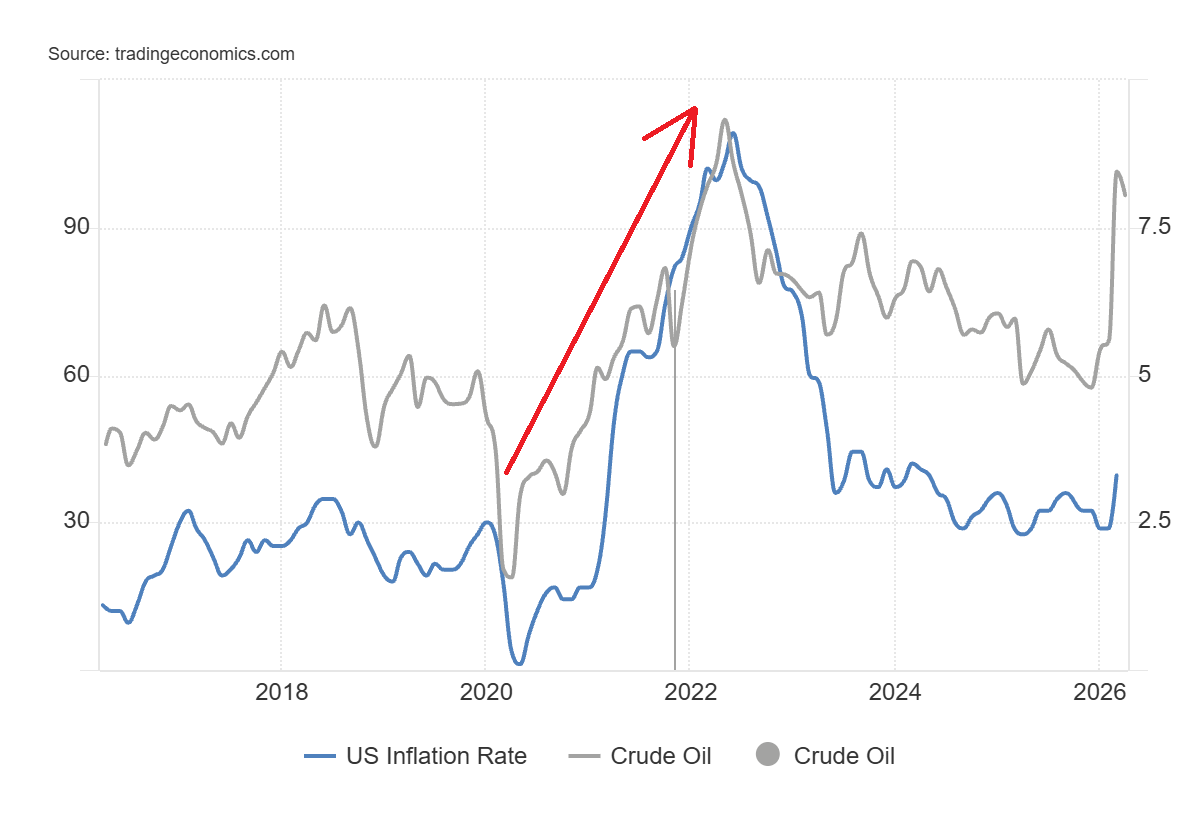

But here's what matters more than the headline: The immediate pressure remains oil. March CPI already showed gasoline accounting for 75% of the headline increase (+21.2% m/m).

Core inflation at 2.6% is contained, but the Fed is boxed in — markets are pricing essentially no cuts through 2026. Meanwhile, earnings season launches this week with banks setting the tone and TSMC testing the AI thesis on Thursday.

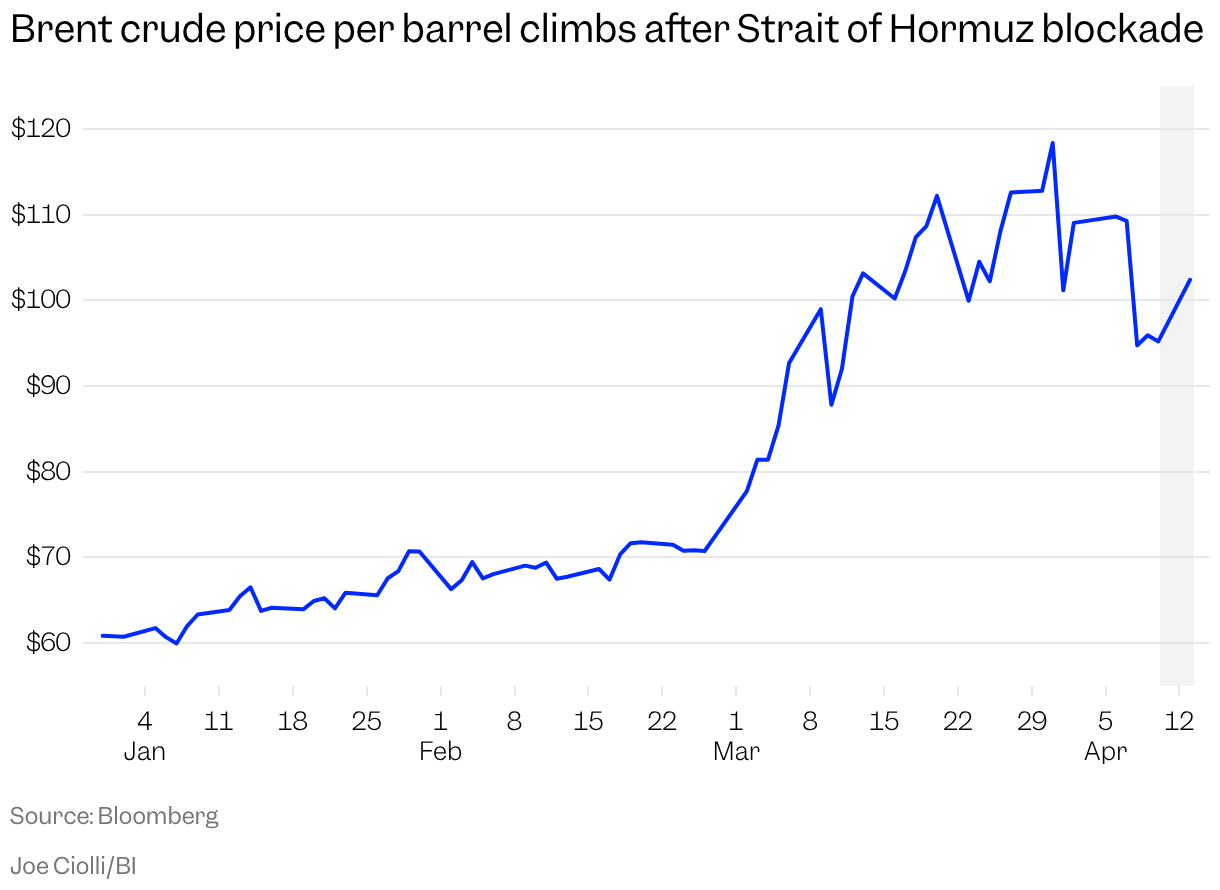

Key Drivers This WeekCeasefire Collapses: US Retakes the Offensive The ceasefire that briefly calmed markets lasted exactly four days. Brent surged 6.9% to $101.79. WTI hit $103.60. Heating oil spiked 8.7%. JPMorgan warns oil could hit $120 if the Hormuz stalemate drags into July. Goldman says another month of closure keeps Brent above $100 for all of 2026.

But Proflex reads the strategic picture differently from the panic pricing.

Proflex View: The ceasefire collapsed but the strategic picture improved. Iran at the table means the war has a ceiling — the question is when a deal lands, not if. The US is controlling the escalation tempo, and the blockade is leverage, not desperation. Oil stays elevated short-term, but this is a negotiating war, not an existential one. Watch for a second round of talks within weeks.

Earnings Season Begins: Banks Set the Tone Goldman Sachs kicked off Q1 earnings Monday with a top-and-bottom-line beat — EPS of $17.55 vs $16.49 expected, revenue of $17.23B. The real test of banks comes Tuesday: JPMorgan, Wells Fargo, and Citigroup all report. - Consumer spending patterns — are households pulling back under $4+ gas prices? S&P 500 Q1 earnings are expected to grow 14% YoY — the sixth consecutive quarter of double-digit growth, the longest streak since 2011 (Nationwide).

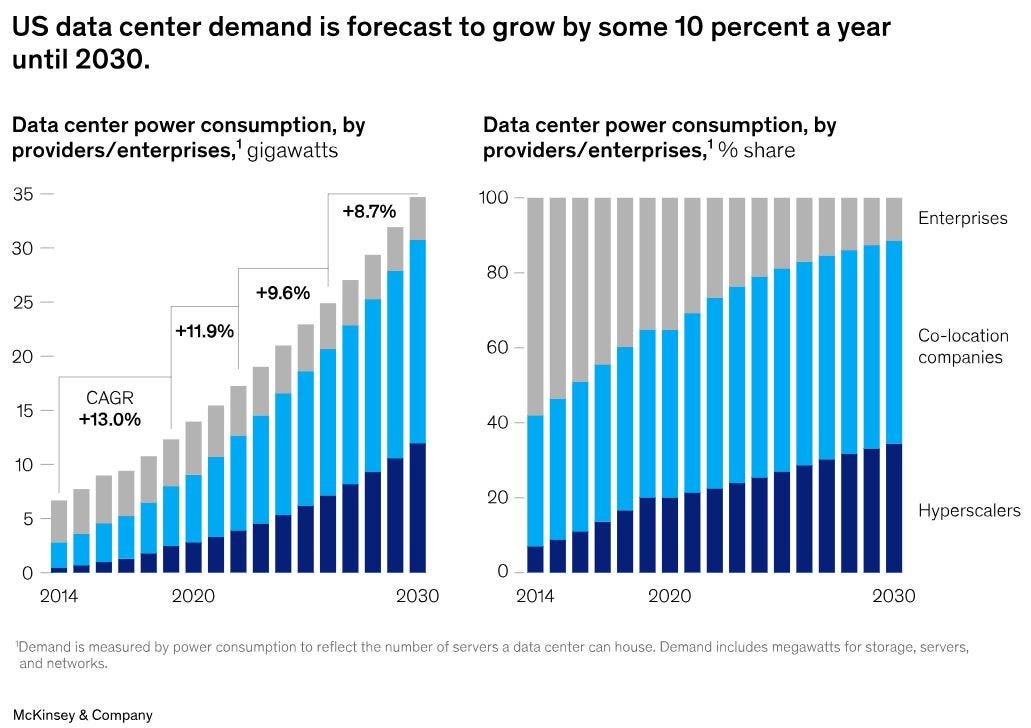

Proflex View: The market needs proof that $100+ oil hasn't broken the consumer or crushed margins. Bank commentary on credit quality and spending patterns will set the tone for the entire season. If guidance holds, the fundamental case for equities remains intact even under war premium. AI's Infrastructure Wall: $650B in Capex, Only 5GW Built The AI trade is priced for exponential growth. The infrastructure to support it tells a different story. Of approximately 16 GW of data center capacity planned for 2026, only 5 GW is actually under construction. The remaining 11 GW hasn't broken ground despite requiring 12–18 months to build. It gets worse further out: of 21.5 GW announced for 2027, only 6.3 GW is under construction. Beyond 2028, almost nothing has broken ground. Money isn't the bottleneck. Hyperscalers have committed $650B+ in capex this year — AWS scaled its Mississippi investment to $25B, TSMC is investing $165B in Arizona chip fabs, and Aligned just broke ground on 540MW in Texas. PJM Interconnection — the grid operator covering 13 states — faces a potential 60GW power shortfall. This creates a two-speed market: operators who've secured power and permits command enormous pricing power, while the rest face multi-year delays.

Proflex View: AI demand is real and accelerating — TSMC's 35% revenue growth and reports of unnamed customers trying to buy ALL of AWS's Graviton capacity confirm that. But, For investors, the bottleneck shifts value from "AI software" to "AI infrastructure enablers" — grid operators, power producers, and industrial suppliers. The secular AI theme has a multi-year runway, but the path runs through physical infrastructure that takes years to build. The Energy-AI Nexus: The Hidden Constraint Rising energy costs are hitting at precisely the moment AI needs more electricity than the grid can provide.

Proflex View: Energy is the hidden constraint on AI growth. Rising oil tightens the grid and compresses margins for data center operators simultaneously. The companies that solve the power problem — through nuclear, on-site generation, or secured long-term contracts — will be the AI winners. The rest are building castles on someone else's electricity. 🔍 What We're Watching

Proflex All-Access: Your Market Compass

Explore the financial markets with Proflex All-Access, your comprehensive resource for deeper market understanding and active participation. This premium service offers subscribers exclusive insights and actionable investment advice, giving you a significant edge in various market conditions.

Proflex All-Access provides detailed analyses and recommendations to optimize your investment strategy. Our specialized newsletters include:

• Growth Gazette (Contains Crypto Pulse) : Aimed at achieving above-market returns for aggressive portfolio growth.

• Income Insider: Focused on conservative strategies and income generation for yield-seeking investors.

ProFlex® by Blockstart Research

Legal Disclosures ProFlex® by Blockstart Research, the premium newsletter product series, provides informational and educational content only and does not offer personalized investment advice or establish a fiduciary relationship. While we rely on reliable sources and research, the information is not tailored to individual financial situations. Readers are urged to consult qualified financial professionals before making investment decisions. We do not guarantee the accuracy, completeness, or timeliness of the information and are not responsible for any investment decisions based on this newsletter. Investing carries risks, and past performance doesn't predict future results. By accessing this newsletter, you acknowledge that we are not liable for actions or decisions resulting from its content. Please conduct due diligence and seek professional advice as needed.

|

Proflex Institutional Research Series

ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.